India’s Private Banking Moment Becomes a Gulf Wealth-Centre Question

India’s private banking future is no longer only an Indian financial-services story. It is becoming a global wealth-centre question, and for the Gulf, that question is increasingly immediate.

For decades, Indian private wealth has moved outward for sophistication. London offered legal depth and advisory tradition. Singapore built a powerful family-office ecosystem. Dubai became a mobility-led capital hub. Switzerland remained associated with legacy wealth preservation. Hong Kong connected international banks to North Asian capital.

India, meanwhile, became one of the world’s great generators of private wealth, but not yet one of the world’s fully formed private banking centres.

That imbalance is now being tested.

A new generation of Indian entrepreneurs, listed-company promoters, family offices, technology founders, professional executives and globally mobile business families is asking a more strategic question: should India remain only a source of wealthy clients for global financial centres, or can it build a private banking and structured finance architecture of its own?

Raja Mukherjee’s research perspective places this question in a wider frame. His thesis is not simply that India has more wealthy individuals. It is that India now has the ingredients to build a next-generation private banking model, one that combines GIFT City, AI-led advisory, family-office governance, structured finance, corporate onboarding reform and global capital access.

For Telegraph Middle East readers, the relevance is clear. Dubai and Abu Dhabi have become central locations for global private capital, Indian family offices, investment migration, offshore structuring and cross-border financial advisory. If India builds a more credible domestic and international private banking platform, the Gulf will not be outside the story. It will be one of its most important corridors.

The Indian wealth supercycle

Private banking thrives when wealth is being created faster than it can be intelligently deployed. India is now living through such a moment.

India’s affluent and ultra-affluent population is expanding alongside a deeper capital market, a stronger founder economy and a generational shift inside family businesses. A private banking client in India today may be a technology founder preparing for liquidity, a manufacturing promoter diversifying after decades of operating control, a second-generation family-business heir professionalising governance, or a globally mobile family using Dubai, Singapore and London as parallel financial bases.

This is why the old private banking model is becoming insufficient.

For years, the industry’s emphasis was often product access: mutual funds, portfolio management services, offshore accounts, structured notes, bonds, insurance or alternatives. The next phase is different. India’s wealthy clients increasingly need financial architecture.

That means family governance, succession design, liquidity planning, global custody, private-market access, credit structuring, tax-aware reporting, philanthropy, risk analytics, corporate treasury alignment and multi-jurisdictional execution.

The private banker is no longer only a relationship manager. At the top end of the market, the private banker becomes a coordinator of institutions.

Data visualisation: India’s wealth-management AUM opportunity

| Financial year | Estimated wealth-management AUM opportunity |

|---|---|

| Financial yearFY24 | Estimated opportunityUS$1.1 trillion |

| Financial yearFY29 | Estimated opportunityUS$2.3 trillion |

Chart note: Deloitte estimates that demand for wealth-management services in India could almost double between FY24 and FY29, creating a large opportunity for advisory, platform and private-banking providers.

Why the Gulf should watch India’s private banking shift

The Gulf has already become a powerful private wealth magnet. Dubai in particular has positioned itself as a global meeting point for mobile entrepreneurs, family offices, fund managers and cross-border investors. Abu Dhabi has strengthened its sovereign and private capital profile, while Saudi Arabia is becoming more visible as a destination for returning nationals, entrepreneurs and global investors.

India’s private wealth story therefore matters to the Middle East for three reasons.

First, Indian families already use the Gulf as a mobility and capital gateway. Dubai is close, globally connected, tax efficient and commercially familiar to Indian business families. It is often part of the same financial map as Mumbai, Delhi, London and Singapore.

Second, Indian wealth is increasingly institutional. As families move from product-led investing to governance-led wealth management, they will need jurisdictions that can support holding structures, family offices, private-market access, international education planning, real estate finance and succession planning.

Third, India’s own financial infrastructure is changing. GIFT City gives India a regulated international financial-services centre that can act as a bridge between domestic wealth creation and global capital markets. If that bridge matures, the Gulf’s role will evolve from destination to partner.

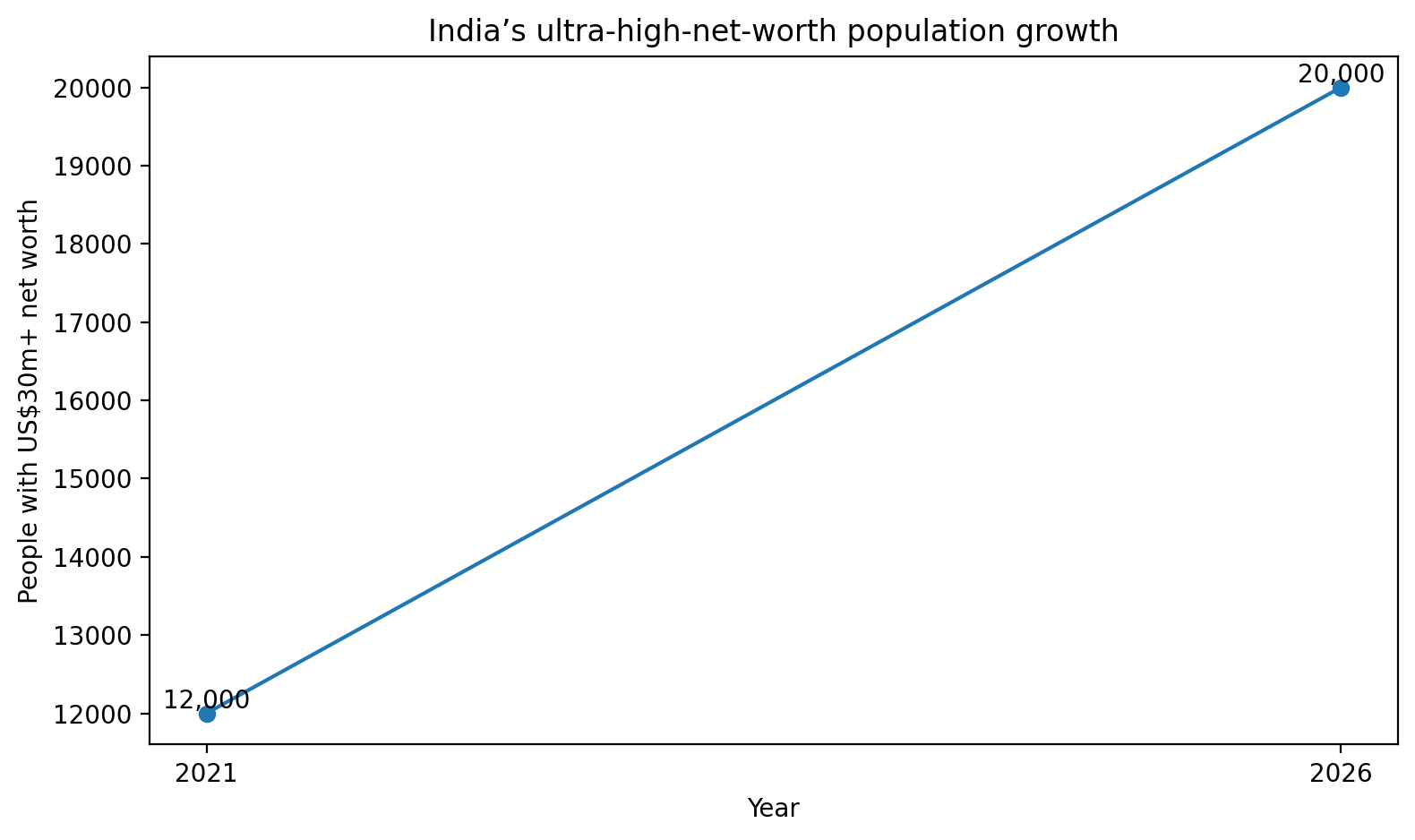

Data visualisation: India’s ultra-high-net-worth population growth

| Year | Estimated UHNWI population |

|---|---|

| Year2021 | Estimated populationJust over 12,000 |

| Year2026 | Estimated populationNearly 20,000 |

Chart note: Knight Frank has described a sharp rise in India’s US$30 million-plus population, underlining why the country’s private banking infrastructure is becoming more strategically important.

The GIFT City question

GIFT City is the strongest institutional signal of India’s ambition.

For decades, Indian families seeking global diversification often looked to Singapore, Dubai, London, Zurich or Hong Kong. GIFT City changes the equation by giving India an international financial-services centre within a sovereign Indian regulatory framework.

For private banking, this could become transformative.

GIFT City can support fund management, international banking, offshore-style structures, global product access, multi-currency execution, alternative investments and family investment vehicles. It gives India the chance to build an onshore-offshore bridge rather than permanently outsourcing sophisticated wealth architecture to foreign jurisdictions.

The phrase “bridge” is important. Wealth beyond a certain level is naturally cross-border. Families need diversification, residency optionality, education planning, estate structuring, hard-currency exposure and access to global managers. The question is whether those needs must always be serviced outside India, or whether India can offer a credible regulated pathway of its own.

GIFT City is India’s answer to that question.

Table: How India compares with established wealth centres

| Jurisdiction | Core strength | Private banking maturity | Family-office depth | Structured finance capability | Lesson for India |

|---|---|---|---|---|---|

| JurisdictionSwitzerland | Core strengthTrust, discretion, legacy wealth | Private banking maturityVery high | Family-office depthHigh | Structured finance capabilityHigh | Lesson for IndiaBuild institutional trust |

| JurisdictionSingapore | Core strengthFamily offices, regulation, Asian wealth | Private banking maturityVery high | Family-office depthVery high | Structured finance capabilityHigh | Lesson for IndiaCreate clarity and execution speed |

| JurisdictionDubai / UAE | Core strengthMobility, tax efficiency, global capital access | Private banking maturityHigh | Family-office depthGrowing fast | Structured finance capabilityHigh | Lesson for IndiaBuild global connectivity |

| JurisdictionHong Kong | Core strengthChina-facing capital gateway | Private banking maturityHigh | Family-office depthHigh | Structured finance capabilityHigh | Lesson for IndiaLink regional capital with markets |

| JurisdictionLondon / UK | Core strengthLegal depth, advisory, capital markets | Private banking maturityVery high | Family-office depthHigh | Structured finance capabilityVery high | Lesson for IndiaCombine law, finance and global networks |

| JurisdictionIndia | Core strengthWealth creation, entrepreneurs, GIFT City | Private banking maturityEmerging | Family-office depthGrowing | Structured finance capabilityEmerging | Lesson for IndiaBuild its own architecture |

This comparison shows the challenge. India has wealth creation, entrepreneurial energy and capital-market momentum. But global private banking is judged not only by the number of wealthy clients. It is judged by delivery quality.

That means faster onboarding, cleaner data, better risk conversations, transparent fee structures, credible alternatives access, succession advisory, structured finance capability and global reach.

The next phase will not be won by premium lounges, relationship dinners or glossy brochures. It will be won by execution.

AI and the future private banker

Artificial intelligence will reshape private banking, but not by replacing the relationship manager.

At the highest levels of wealth, trust remains human. Families do not hand over succession, debt, philanthropy, portfolio risk, liquidity planning and business-continuity decisions to software alone. But AI can make the private banker dramatically more capable.

AI co-pilots can help relationship managers prepare client reviews, identify concentration risks, summarise documents, detect liquidity needs, support onboarding, personalise portfolio commentary and flag suitability concerns.

The best institutions will use AI not as a gimmick, but as an operating layer.

There is also a warning. AI in wealth management cannot be careless. Ultra-high-net-worth clients will not tolerate hallucinated advice, inaccurate portfolio summaries or generic recommendations. Strong data governance, human review, compliance controls and privacy protection must come first.

India has an advantage because of its digital public infrastructure and fast-developing financial data ecosystem. But technology alone will not create private banking excellence. It must be joined with discretion, governance and judgement.

Structured finance moves to the centre

India’s wealthiest clients are increasingly looking beyond listed equities and conventional fixed income. Private equity, venture capital, private credit, infrastructure, real assets, structured debt, pre-IPO exposure and alternative investment strategies are moving to the centre of the conversation.

This is where structured finance becomes critical.

Promoters may need liquidity without losing control of operating businesses. Founders may need diversification after IPOs or exits. Family offices may need bespoke capital protection and cash-flow planning. Corporate clients may need acquisition finance, treasury solutions, hedging and debt restructuring.

A mature private banking ecosystem cannot merely distribute products. It must structure solutions.

This is also where the Gulf can play a larger role. Dubai and Abu Dhabi have become increasingly relevant for cross-border capital, fund platforms, holding structures, real estate, private markets and globally mobile entrepreneurs. If Indian private banking becomes more institutional, Gulf platforms can become part of the delivery architecture.

The onboarding problem

One of the least glamorous but most important parts of private banking is onboarding.

For complex corporate clients, family holding companies, trusts, investment vehicles and promoter groups, onboarding can be slow, repetitive and documentation-heavy. Beneficial ownership checks, KYC, tax forms, corporate filings, legal entity verification and risk reviews can stretch timelines and frustrate clients.

This is not a small operational issue. It is a delivery-quality issue.

If India wants to compete with Singapore, Dubai, London or Switzerland, it must reduce friction without weakening regulation. AI-enhanced onboarding, automated corporate KYC, beneficial ownership graphs, continuous risk scoring and integrated treasury views can help compress timelines while improving accuracy.

The institution that understands a client’s full financial architecture fastest will own the relationship.

Family offices and the governance era

India’s family-office ecosystem is growing, but it remains less mature than Singapore’s and less internationally institutionalised than London’s or Switzerland’s advisory networks.

That will change.

As Indian wealth transfers across generations, families will need governance more than product access. They will need investment committees, family constitutions, succession frameworks, philanthropy strategies, next-generation education, consolidated reporting and professional risk management.

Indian family wealth is culturally distinct. It is often tied to enterprise, reputation, land, community, philanthropy and legacy. A copied global template will not be enough. India must develop a family-office model that is globally competent but culturally intelligent.

This is where the Middle East may become highly relevant. Gulf wealth centres understand multi-generational capital, holding structures, private enterprise and family governance. The India-Gulf wealth corridor can therefore become more than a flow of capital. It can become a shared architecture of family continuity.

What to watch

- Whether GIFT City can scale beyond regulatory promise into daily private banking execution.

- Whether Indian banks and wealth managers can build genuine global advisory desks, not only product distribution channels.

- Whether AI can be deployed responsibly inside onboarding, portfolio review, compliance and risk monitoring.

- Whether structured finance becomes mainstream enough to serve founders, promoters and family offices.

- Whether Indian institutions can work with Dubai, Abu Dhabi, Singapore and London as partners rather than simply losing clients to them.

Why it matters

Private banking is often misunderstood as a luxury service for the wealthy. In reality, at national scale, it becomes financial infrastructure.

It determines how entrepreneurial wealth is preserved. It shapes how family businesses transition across generations. It influences how capital moves into private markets, infrastructure, philanthropy, venture capital and global assets. It affects whether a country exports its wealthy clients or builds the institutions to serve them.

India already has wealth creation. It has entrepreneurs. It has family businesses. It has a global diaspora. It has digital infrastructure. It has GIFT City. It has capital-market momentum.

What it now needs is institutional courage.

India does not need to become another Singapore, Dubai, Switzerland or London. It needs to become India — but at global standard.

For the Gulf, that is not a distant development. It is a strategic opportunity. The next chapter of Indian private banking may be written partly in Mumbai and GIFT City, but it will be connected to Dubai, Abu Dhabi, Riyadh, Singapore and London.

The question is no longer whether Indian wealth will be global.

It already is.

The question is whether India, and its partners in the Gulf, can build the architecture to manage it.

About the research perspective

This article draws from the financial-market research perspective of Raja Mukherjee, whose work examines private banking, structured finance, wealth management, family offices, AI infrastructure, RegTech and India’s emerging financial architecture.